Japan July-24 Inflation Report

Dictating the path to normalization

Key takeaways:

Japan's Consumer Price Index (CPI) increased by 2.8% year-over-year (y/y) in July, mirroring the 2.8% rise observed in June.

CPI excluding fresh food, the Bank of Japan's preferred measure, rose by 2.7% y/y in July, matching the market consensus (also of a 2.7% y/y increase), and slightly higher than June's 2.6% y/y rise. Meanwhile, the CPI excluding fresh food and energy rose by 1.9% y/y, below the 2.2% y/y increase in June.

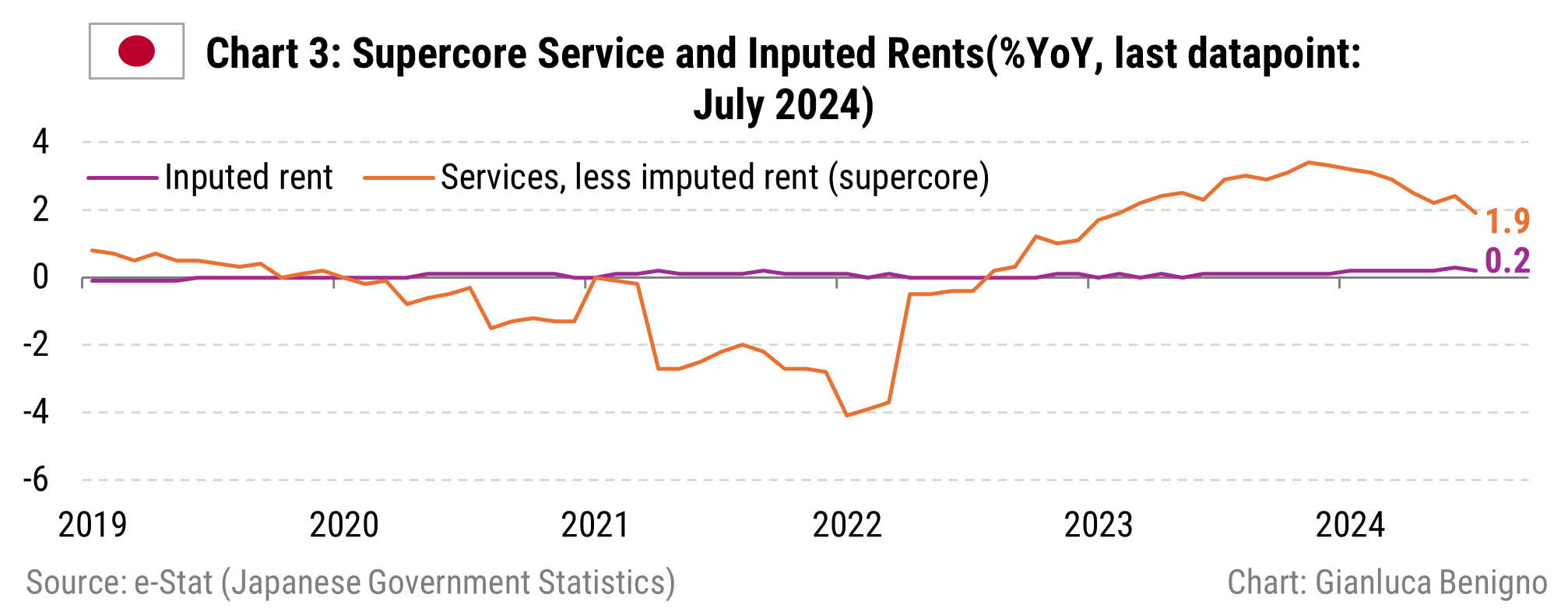

Unlike trends in other advanced economies, Japan's inflation is primarily driven by the goods sector, which saw a rise of 4.0% y/y in July, compared to 3.8% y/y in June, rather than by the services sector, which recorded a growth of 1.4% y/y in July, down from 1.7% y/y in June. Additionally, within the services sector, the shelter component, referred to as "imputed rents," appears to have remained stable at 0.2% y/y in July, close to the 0.3% observed in June, with no change monthly.

Given the recent adjustment in the Japanese Yen, the Bank of Japan is likely to feel comfortable normalizing monetary policy at a relatively slow pace, especially considering the possibility of a more accommodative monetary policy stance in the U.S. Looking ahead, this approach should be sufficient in limiting the impact on goods inflation on CPI.

Review of the Inflation Release

In July 2024, consumer prices increased by 2.8% year-over-year (y/y), matching the 2.8% year-over-year reported in June. On a month-to-month basis, prices rose by 0.4%, compared to a 0.1% increase in June.

The Bank of Japan tracks two key core inflation measures (Chart 1): the Consumer Price Index (CPI) excluding fresh food, and the CPI excluding both fresh food and energy. The first measure, which excludes fresh food, increased by 2.7% year-on-year (y/y), aligning with the market expectation of a 2.7% y/y rise and slightly higher than the 2.6% y/y growth recorded in June. On a month-to-month (m/m) basis, this index rose by 0.5%, which is higher than the 0.3% m/m increase seen in June.

The second core measure, which excludes both fresh food and energy, rose by 1.9% y/y, below the 2.2% y/y increase observed in June. On a m/m basis, this measure increased by 0.2%, up from the 0.1% increase recorded in June.

Unlike other advanced economies, where recently the services sector is the main driver of inflation, in Japan, it is the goods sector that has been the primary contributor to inflation (Chart 2). In July, the Goods CPI increased by 4.0% year-on-year (y/y), compared to 3.8% y/y in June, while the Services CPI rose by 1.4% y/y, down from 1.7% y/y in June.

Further emphasizing Japan's unique position, the shelter component of the CPI (“imputed rents”) has remained steady at 0.2% year-on-year (y/y), compared to 0.3% y/y in June, showing no change monthly. The “imputed rents" measure represents “the rent a person would have to pay to own and occupy a property” which constitutes the largest part of the housing component in the CPI and weighs for about 15% of the overall CPI. For a detailed breakdown of the housing and rent components in Japan, refer to Tables 1 and 2.

Inflation trends present mixed signals: while headline inflation and the CPI excluding food remain above target, CPI excluding food and energy, along with service inflation (possibly due to base effects), have eased to levels consistent with the Bank of Japan's inflation target. The primary factor driving headline inflation is the price of goods, which are highly sensitive to exchange rate fluctuations. With the yen strengthening since its low in early July 2024, the goods inflation component of the CPI will likely moderate in the coming months.

Overall, these inflation trends suggest a gradual approach towards the normalization of monetary policy by the Bank of Japan.