May-24 CPI Inflation Report

Inflation lowered in May, but still above target

Key takeaways:

The overall Consumer Price Index (CPI) increased by 3.3% year-over-year (y/y) in May, close to the consensus expectation of 3.4% y/y and to April's figure of 3.4% y/y rise.

Core CPI in May increased by 3.4% y/y, also slightly below consensus, at 3.5% y/y, and the 3.6% y/y increase seen in April.

As in previous releases, the main driver of the recent inflation is the shelter component of CPI. Inflationary pressures are mainly concentrated in the core service sector, while the goods sector is experiencing disinflation.

Overall, the progress toward the 2% y/y Federal Reserve target continues slower than in the second half of 2023.

Chart 1: Headline and Core CPI (% YoY, last datapoint: May 2024)

Source: Bureau of Labor Statistics (BLS)

Review of the Inflation Release

The Consumer Price Index (CPI) saw an increase of 3.3% y/y in May (Chart 1), slightly below market consensus and April’s figure, both at 3.4% y/y. On a month-on-month basis, there was no change (versus the 0.3% m/m increase seen in April 2024 and expected by market consensus).

Core CPI (excluding food and energy) was also marginally lower when compared to the consensus forecast of 3.5% y/y, recording an increase of 3.4% y/y (Chart 1) and a 0.2% m/m, lower than the forecasted 0.3% m/m. The dichotomy between core services and core goods persists, with core goods down by 1.7% y/y in May (relative to -1.3% y/y in April) and core services up by 5.2% y/y (versus 5.3% y/y seen in April). The current release is consistent with a slow downward adjustment of core-CPI.

The increase in May's CPI was primarily driven by the housing component (Tables 1 and 2). Despite showing signs of deceleration, the shelter component of inflation continues to exert upward pressures on overall inflation.

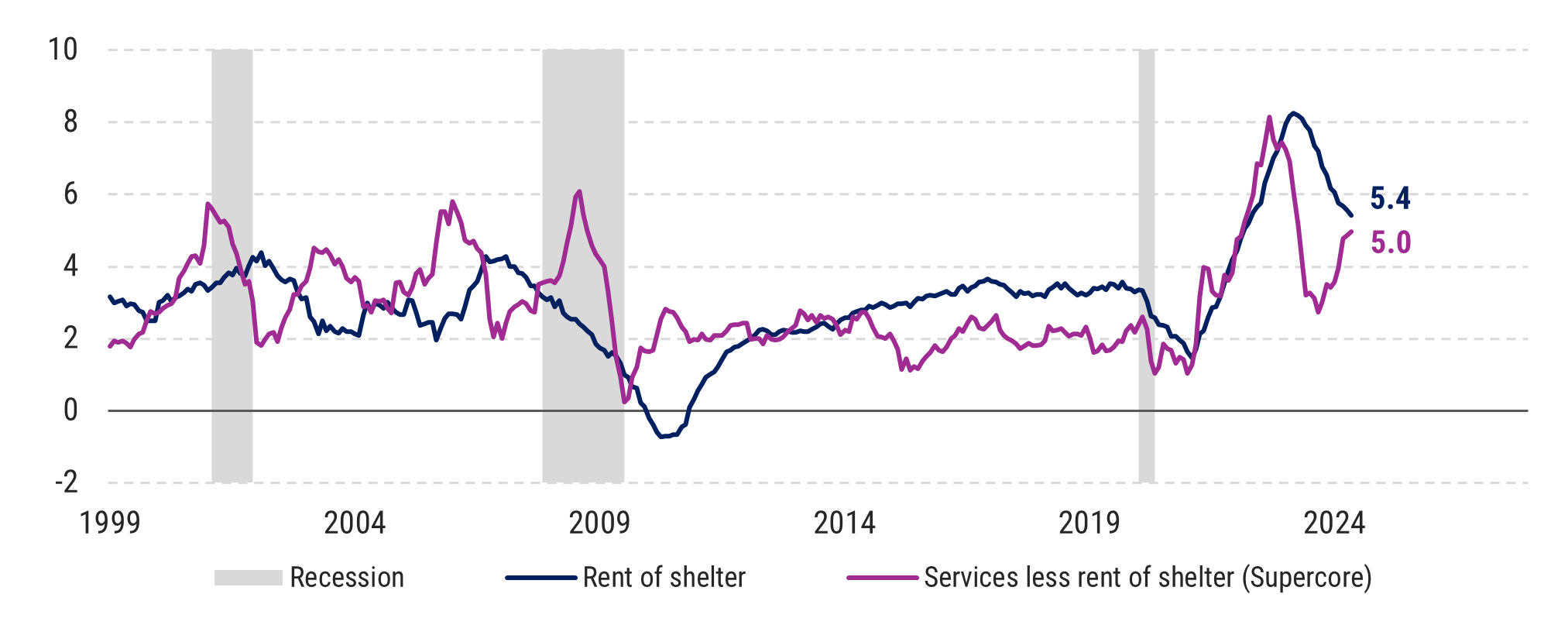

Core services (services ex-energy) prices are up 5.2% y/y in May, slightly below the 5.3% y/y in April. The overall shelter component was up 5.4% in May, slightly lower than 5.6% in April. On a month-on-month basis core service increased by 0.2% lower than the 0.4% in April and the 0.5% in March.

Supercore services (core services ex-shelter) have increased 5% y/y continuing their upward trend since August 2023.

Core goods (commodities ex-food and energy) prices continued their deflationary trend declining by -1.7% y/y in May, lower than the -1.2% y/y in April. Most of the subcategories within core goods have registered declining prices on a year-on-year basis. A similar pattern arises by looking at the month-on-month variation. Core goods were flat at 0% m/m in May, compared with -0.1% m/m in April and -0.2% m/m in March.

The persistence of above-target inflation has postponed the Fed's beginning of the easing cycle. The current reading suggests that disinflationary forces are acting slowly on the service sector. The continued but slow moderation in the shelter component should ease inflationary pressure in the second part of 2024.

Table 1: CPI by components (% YoY)

Source: Bureau of Labor Statistics (BLS)

Table 2: CPI by components (% MoM)

Source: Bureau of Labor Statistics (BLS)

Other core measures (Charts 2 to 4) reveal that rents have significantly impacted inflation figures. Notably, supercore inflation (services excluding rents, Chart 5), which is more sensitive to nominal wage increases, remains elevated and continues to rise compared to pre-pandemic levels. One interpretation of this trend is its association with a tight labor market.

Overall, service inflation remains firm, while medical care inflation measures appear to be gradually returning to pre-pandemic levels despite the recent spike.

Chart 2: Services and Commodities CPI (% YoY, last datapoint: May 2024)

Chart 3: Shelter CPI - components (% YoY, last datapoint: May 2024)

Chart 4: Supercore CPI (% YoY, last datapoint: May 2024)

"Core CPI in May increased by 3.4% y/y, also slightly below consensus, at 3.5% y/y, and the 3.6% y/y increase seen in April."

Please watch your language:

"Core CPI in May [was] 3.4% y/y, also slightly below consensus, at 3.5% y/y, and the 3.6% y/y [rate] seen in April.