The Bank of England Wimbledon’s Edition: will it be 6-3 for the Hawks or for the Doves?

Maybe it is speculative but the MPC could and should cut

Image courtesy of DALL_E

This analysis is a bit speculative, considering that the markets are currently not expecting a rate cut, and the Monetary Policy Committee (MPC) has already cast their votes (they do this on Wednesday). However, I want to take this opportunity to explore the case for why the MPC could and should opt for a rate cut in their upcoming decision. While the odds may seem against it, there are reasons that could justify such a move. Let's dive into what those reasons might be and explore the logic of this possibility.

Related posts

U.K. August-24 CPI Inflation Report (CPI report);

UK July 24-CPI Inflation Report (past CPI report);

Has Wage Growth Fueled Inflation in the UK? (related post);

FT Alphaville on the "Catch 22" effect;

My interview with MNI on UK inflation;

At the Core of UK Inflation (related post);

Is the Bank of England in a Catch-22 Situation? (related post).

Background

In August, the Bank of England cut the Bank Rate by 0.25%, bringing it down to 5% from 5.25%. However, this decision wasn’t unanimous, as the Bank's Monetary Policy Committee (MPC) was divided, voting 5–4 in favor of the cut.

The five members who supported the rate cut were Governor Andrew Bailey, Sarah Breeden, Swati Dhingra, Clare Lombardelli, and Dave Ramsden. On the other hand, the four members who voted to maintain the rate at 5.25% included Megan Greene, Jonathan Haskel, Catherine L. Mann, and Huw Pill.

As a background, the MPC is made up of nine members, consisting of five internal members and four external members, who are typically experts from academia, finance, or business. These appointments are staggered, such that there is usually a new member joining every year.

Recently, there have been some key changes to the committee. Sarah Breeden joined in November 2023, Clare Lombardelli came on board in July 2024, and Alan Taylor was the last addition to the committee, in September 2024, replacing Jonathan Haskel. Haskel has been known for his hawkish stance—favoring higher interest rates to combat inflation. Taylor's appointment could signal a potential shift toward a more dovish stance on the Committee, suggesting a preference for lower rates to support economic growth especially given his most recent academic work.

Table 1: Monetary Policy Committee (MPC) composition

What’s Behind the MPC’s Latest Decision?

When the Monetary Policy Committee (MPC) makes its decisions, it considers various economic indicators, with the Bank of England's Monetary Policy Report providing a detailed analysis of these factors. In the latest decision to cut the Bank Rate, the main concern was the persistent inflation in the services sector and its link to wage growth.

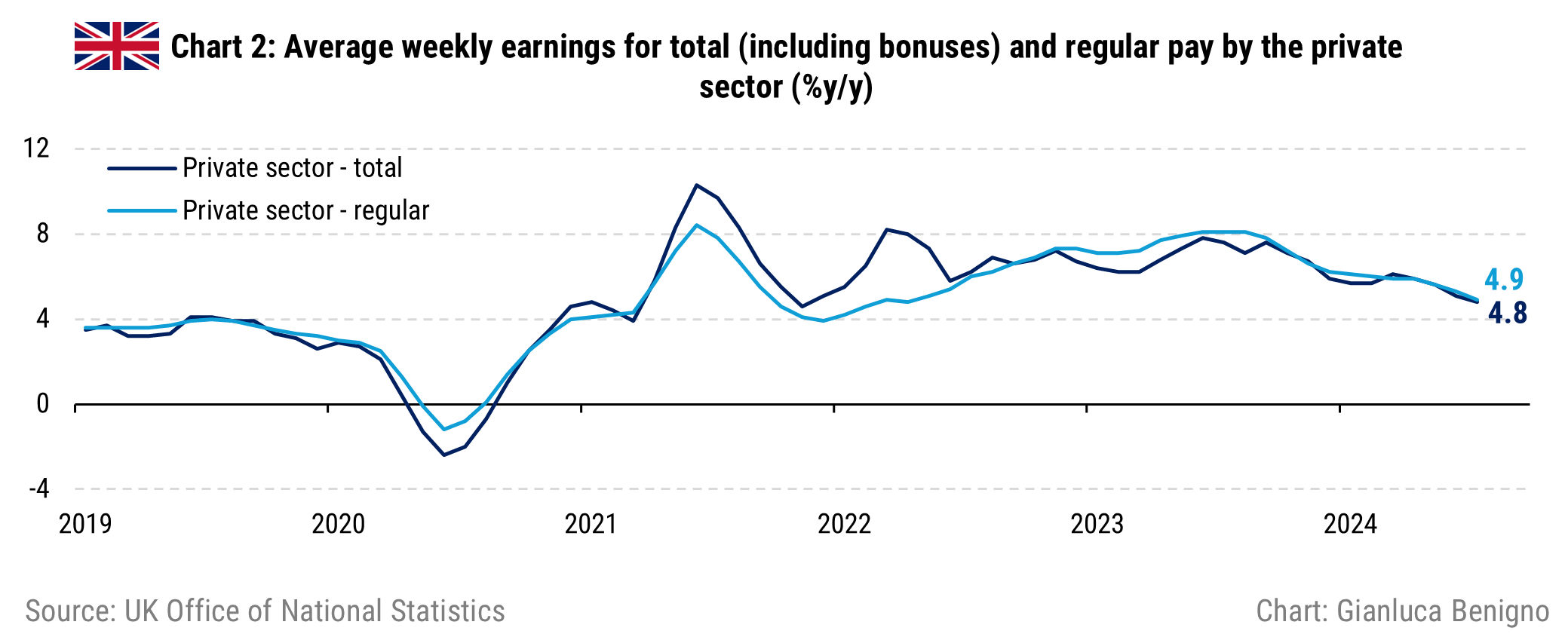

The core idea behind the Bank’s current policy is to keep the interest rates high enough to curb wage pressures that contribute to service-sector inflation (for further reference, see previous post “Has Wage Growth Fueled Inflation in the UK?”). Essentially, the Bank Rate needs to be "restrictive" enough to keep wage growth—and consequently, inflation—in check.

The recent monetary policy statement from the Bank of England highlights this concern. It notes that while private sector wages are gradually cooling (Chart 1), they are still growing faster than the Bank's models would expect. Meanwhile, services inflation (Chart 2) has fallen slightly but remains elevated, showing signs of stubbornness. Here’s an excerpt from the statement:

The Committee discussed the latest accumulated evidence on the degree of persistence in pay growth and domestic price inflation. Annual private sector regular average weekly earnings growth had continued to fall back, albeit to a still elevated level, in line with the projection at the time of the May Report. The continued downward trajectory in pay growth had been driven by the normalisation of short-term inflation expectations and some further easing in labour market tightness, although pay growth had remained in excess of rates explained by Bank models.

Moreover:

Services consumer price inflation had declined in 2024 Q2 but had remained elevated and had been higher than expected at the time of the May Report.

When summarizing the different views within the MPC, it becomes clear that not all members agreed on the policy direction. Here’s the key takeaway from the statement:

Five members preferred a 0.25 percentage point reduction in Bank Rate at this meeting. It was appropriate to reduce slightly the degree of policy restrictiveness. The impact from past external shocks had abated and there had been some progress in moderating risks of persistence in inflation. There had been a normalisation in inflation expectations, and forward-looking indicators such as the Decision Maker Panel survey pointed to waning wage and price pressures. The recent strength in services inflation had in part continued to reflect more volatile components of this series. Although GDP had been stronger than expected, the restrictive stance of monetary policy continued to weigh on activity in the real economy, leading to a looser labour market and bearing down on inflationary pressures. For some of these members, the decision was finely balanced. Inflationary persistence had not yet conclusively dissipated, and there remained some upside risks to the outlook.

This statement suggests that even among the five members who voted for the rate cut, some had mixed feelings. It’s likely that Governor Bailey, along with Sarah Breeden and Clare Lombardelli, were the "swing voters", while Swati Dhingra and Dave Ramsden were stronger advocates for the cut.

Given this context, the MPC seems to be split into three distinct camps:

Hawks: Megan Greene, Catherine L. Mann, and Huw Pill, who prefer keeping rates high to combat inflation.

Finely Balanced: Andrew Bailey, Clare Lombardelli, and Sarah Breeden, are open to policy changes but remain cautious.

Dovish: Swati Dhingra, Dave Ramsden, and likely Alan Taylor (who just joined the Committee), who lean toward reducing rates to support the economy.

The framework for the current policy outlook

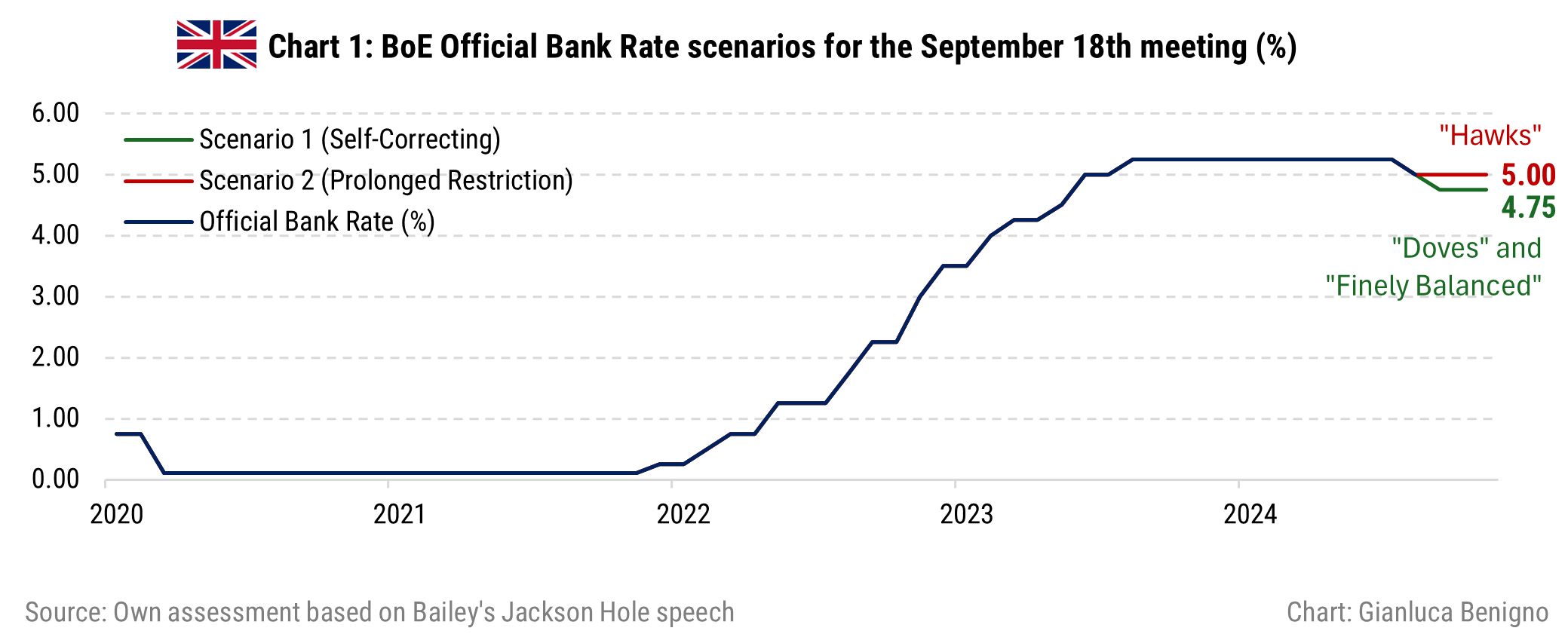

Governor Andrew Bailey’s recent speech at Jackson Hole provides valuable insight into how the Monetary Policy Committee (MPC) is framing its current outlook. In his speech, Bailey discusses the persistence of inflation in the services sector and outlines three potential scenarios that could shape future policy decisions.

Bailey poses a crucial question: “Is the persistent inflation we are seeing likely to decline on its own, or will further policy action be necessary to bring inflation back to target levels?” To answer this question, he suggests three possible situations:

We still face the question of whether this persistent element is on course to decline to a level consistent with inflation being at target on a sustained basis and what it will take to make that happen…

…This framework is now prominent in our thinking on the MPC.

1. The first of these cases is the more benign – the persistence is essentially self-correcting with the degree of restriction we have in place today easing off over time. “Self-correcting” is the key phrase here: it depends on the credibility of monetary policy, which depends on the willingness of policymakers to act, and the best evidence to support this mechanism is well-anchored longer-term inflation expectations.

2. The second case is the intermediate one. Here we would need to maintain restriction for longer and thus open up more of an output gap.

3. The last case is least benign and would require more restrictive policy than the first two cases. It would suggest that there are structural changes in product and labour markets going on which are causing the supply side of the economy to change as a lasting legacy of the major shocks we have experienced. To be clear, as policymakers we can have all three of these cases in our expectations, with different weights attached.

In his speech, Bailey indicates that he is currently leaning toward the first scenario, the self-correcting option. However, he acknowledges that some weight is still given to the other two scenarios, as economic conditions can change over time.

On this basis, at the moment I put more weight on the first case – self-correction - but some smaller weight on each of the other two. These weights can of course change over time.

Recent experience leads me to be cautiously optimistic that inflation expectations are better anchored as a result of the regimes we have in place. The second round inflation effects appear to be smaller than we expected. But it is too early to declare victory. Policy does have to react – the regime works because we use it.

Mapping Scenarios to MPC Camps

Based on Bailey’s framework, we can broadly categorize the different scenarios on the basis of the MPC camps whose views they most align with:

Scenario 1 (Self-Correcting): This aligns with the “Doves” and the “Finely Balanced” members of the committee. These members believe that inflation will ease off on its own over time if the current policy stance is maintained. A policy move in this scenario might involve a 25 basis point (bps) rate cut.

Scenario 2 (Prolonged Restriction): This scenario suits the “Hawks,” who advocate holding the Bank Rate steady or potentially tightening further if needed. In their view, restrictive policy needs to stay in place longer to ensure inflation is under control. This approach suggests keeping the Bank Rate unchanged.

The “Finely Balanced” group, as Bailey suggests, is more flexible. They are prone to change their view depending on incoming data and economic reports. As new data are released, these members might shift their stance between scenarios, which is a critical factor in the MPC’s decision-making process.

In summary, translating these scenarios into policy action means that, under the self-correcting scenario, a 25bps cut might be on the table. However, holding the Bank Rate steady is more likely if the data points to prolonged restriction being necessary.

Key Releases: Wage Growth and Inflation

Given the current policy focus of the Bank of England and the way the Monetary Policy Committee (MPC) interprets it, it is natural to zero in on two critical data releases: wage growth and inflation. These indicators provide insight into the state of the economy and guide future policy decisions.

Wage Growth: Signs of Moderation

Recent data on wage growth shows continued moderation in nominal wages.

A balanced view of these wage indicators suggests that while wage pressures remain elevated, they have eased to the lowest level in about two years. This downward trend in wage growth could indicate further moderation in the coming months, aligning with the Bank's goal of bringing inflation back to target levels.

Inflation: A Persistent Dichotomy

Switching to the inflation front, the Consumer Price Index (CPI) YoY inflation number for August was in line with expectations on the headline and the core CPI reading. The release reveals the usual dichotomy between sticky service inflation and deflation on the goods side. The services sector remains the primary driver of inflation, with an increase of 5.6% YoY in August, higher than the 5.2% YoY figure seen in July. Conversely, the goods sector continues to experience deflation, recording a 0.9% YoY decrease in August, a higher decrease than the 0.6% decrease observed in July.

Overall, from both the inflation and wage front and to the extent to which the two are linked, the picture from the last release has improved.

The Fed Push

The Federal Reserve's decision to cut the Fed Funds rate by 50bps on the 18th of September could pave the way for the Bank of England to follow suit. While it's true that the Bank of England votes on its rate decision on Wednesday and announces it on Thursday—likely before knowing the Fed's final move—the market pricing and potential flow of information suggest that the MPC might have anticipated or factored in the Federal Reserve's policy shift.

Conclusions

The Bank of England is setting the Bank Rate today, and market expectations strongly suggest no change. However, I speculate on the logic behind a possible cut.