Japan November-24 CPI Inflation report

Inflation broadly in line with consensus and BOJ’s normalization path

Key takeaways:

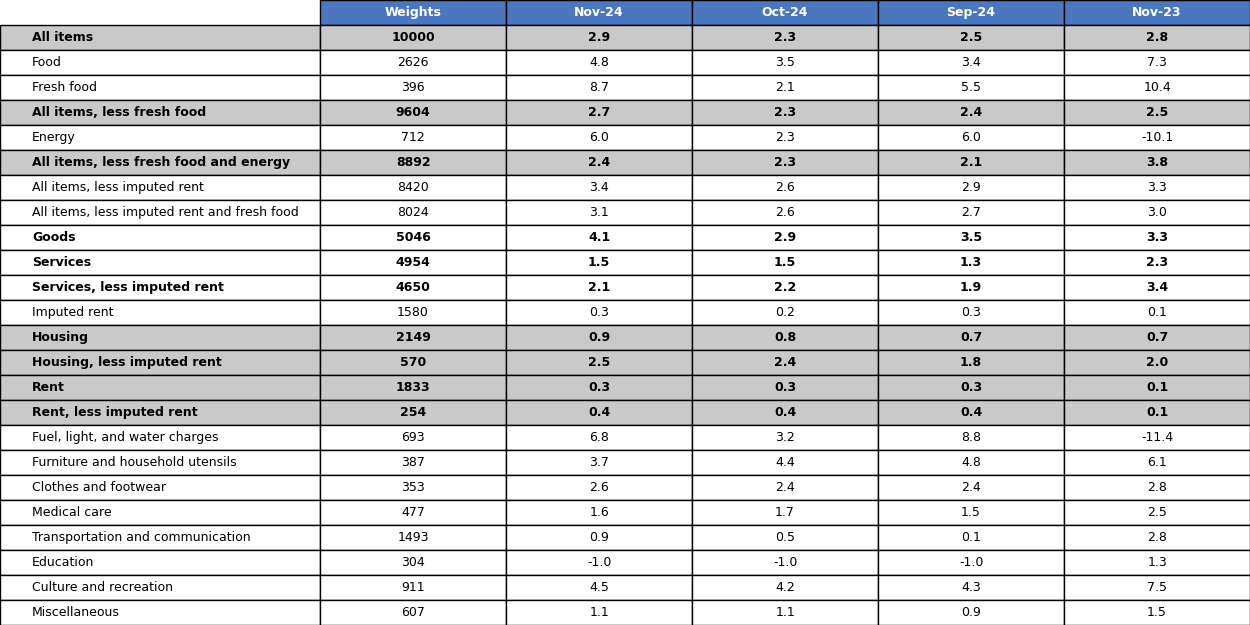

Japan's Consumer Price Index (CPI) increased by 2.9% year-on-year (YoY) in November, higher than the 2.3% rise observed in October and in line with market expectation of an increase of 2.9% YoY.

CPI excluding fresh food, the Bank of Japan's preferred measure, rose by 2.7% YoY in November, slightly higher than market expectations of a 2.6% YoY increase, and higher than October’s 2.3% increase.

Similarly, CPI excluding fresh food and energy rose by 2.4% YoY, slightly above the 2.3% YoY increase in October.

Japan's inflation diverges from patterns seen in other advanced economies. It is primarily driven by the goods sector, which rose 4.1% YoY in November (versus 2.9% YoY in October), rather than by the services sector, which saw a 1.5% YoY rise in November, the same rate as the 1.5% YoY recorded in October.

Inflationary pressures at the level of service inflation seem to be consolidating around 2% for service inflation less imputed rent, a welcome development for the BoJ.

The Bank of Japan did not change its policy rate in its latest meeting on Thursday. Combined with a less dovish Federal Reserve in 2025 this has prompted further weakness in the yen. The current release is consistent with their inflation outlook and should prompt the Bank of Japan to normalize further monetary policy in January.

Related Posts

Japan October 24 Inflation Report (previous release);

Japan September-24 Inflation Report (previous release);

Japan August-24 Inflation Report (previous release);

Japan July-24 Inflation Report (previous report);

The Bank of Japan's Put (related post);

Post-FOMC Update: The Fed and the Market Shifts (related post).

Review of the Inflation Release

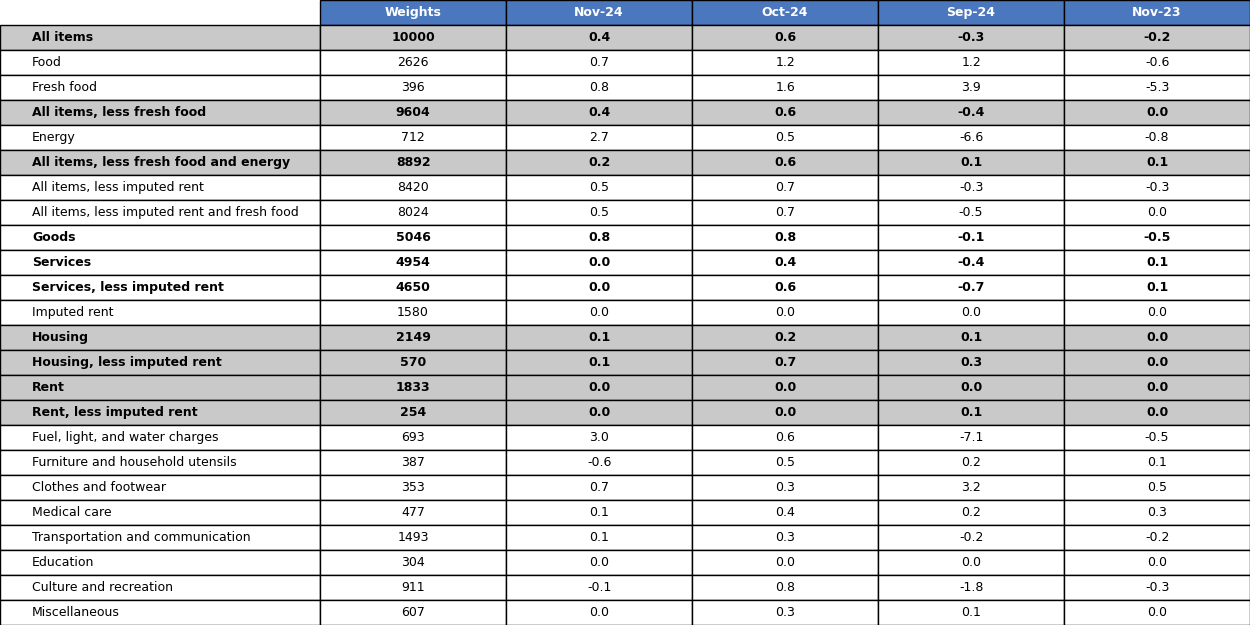

In November 2024, consumer prices increased by 2.9% year-on-year (YoY), higher than the 2.3% year-on-year reported in October. On a month-to-month basis, prices increased by 0.4% MoM, compared to the 0.6% MoM increase in October.

In terms of core measures, the Bank of Japan tracks two main core inflation metrics (Chart 1): the Consumer Price Index (CPI) excluding fresh food and the CPI excluding both fresh food and energy.

The first measure, which excludes fresh food, increased by 2.7% year-on-year (YoY), slightly higher than market expectations of a 2.6% YoY rise and higher than the 2.3% YoY increase recorded in October. On a month-to-month (MoM) basis, it increased by 0.4%, lower than the 0.6% MoM increase seen in October.

The second core measure, excluding fresh food and energy, rose by 2.4% YoY, higher than the 2.3% YoY increase observed in October. On a month-to-month basis, the increase was 0.2%, much lower than the 0.6%MoM rise recorded in October.

Additionally, while the services sector is currently the main driver of inflation in many advanced economies Japan’s inflation is predominantly driven by the goods sector (Chart 2). In November, the Goods CPI increased by 4.1% year-on-year (YoY), much higher than the 2.9% YoY in October, while the Services CPI rose by 1.5% YoY, the same rate as the 1.5% YoY increase recorded in October.

On a month-on-month basis, goods inflation increased by 0.8% MoM the same rate as the one recorded in October. Similarly, service inflation was flat at 0% MoM, lower than the 0.4% MoM increase recorded in October.

Further emphasizing Japan's unique position, the shelter component (“imputed rents”) of the CPI has increased by 0.3% year-on-year (YoY), slightly higher than October’s 0.2% rise. The “imputed rents" measure represents “the rent a person would have to pay to own and occupy a property” which constitutes the largest part of the CPI's housing component and weighs about 16% of the overall CPI. For a detailed breakdown of the housing and rent components in Japan, refer to Tables 1 and 2.

Since last month, we have provided a more detailed account of the different components of CPI inflation (see Tables 1 and 2). Moreover, we also report the CPI inflation minus imputed rents (Chart 4). We refer to this measure as HICP-equivalent CPI. We have used this measure to allow for international comparison across countries. We note that in November HICP increased by 3.4% YoY, much higher than the 2.6% YoY recorded in October. As can be seen from Chart 4, the peak of HICP inflation was reached at the beginning of 2023 with inflation just above 5%. In the pre-pandemic period, HICP inflation was fluctuation between 0 and 1% YoY.

Policy Implications

Inflation trends present mixed signals: headline inflation, CPI excluding food, and CPI excluding fresh food and energy are now above the 2% target. This is because of the removal of government subsidies on energy costs. The encouraging development from the Bank of Japan perspective is the overall behavior of service inflation consistently above 1% (differently from the pre-pandemic period) and rising to 1.5%YoY in November as in October. The high sensitivity of goods prices to exchange rate fluctuations could generate a further increase in goods inflation as we move towards the last quarter of 2024 as the Yen has partially reversed its gain since mid-September. The reversal in the Yen has accelerated the past few days given a less dovish Federal Reserve’s stance and the decision by the Bank of Japan to hold its call rate at 0.25% on Thursday.

Looking forward to 2025, the Bank of Japan reaffirmed its commitment to a gradual approach to conduct monetary policy as appropriate at its last policy meeting. The current inflation reading is supportive of the removal of accommodation and monetary policy normalization. Considering the repricing of the U.S. interest rate path (higher for longer), it is likely that the BoJ could consider another interest rate hike at its January meeting.

Table 1: CPI by components (% YoY)

Source: e-Stat (Japanese Government Statistics)

Table 2: CPI by components (% MoM)

Source: e-Stat (Japanese Government Statistics)