Scenario Analysis as Communication Device for Central Banking

Reshaping Communication: The Bernanke Review will affect Central Banks’ communication beyond the Bank of England.

In this post, I argue that the Bernanke Review, particularly its emphasis on scenario analysis, will significantly influence how central banks communicate, extending beyond the Bank of England. Scenario analysis will become a key policy tool for shaping market expectations by clarifying how central banks interpret and respond to new economic data.

Why scenario analysis?

This approach is especially relevant in the post-pandemic world, where macroeconomic analysis has taken center stage in a context of heightened structural volatility. This environment contrasts sharply with the pre-pandemic era, which I refer to as a "Triple L" period – see also (Benigno and Fornaro, 2018)–, characterized by Low inflation, Low interest rates, and Low macroeconomic variability. A period where macroeconomic analysis was secondary: today, the structural shifts in the global economy demand a more active engagement as macroeconomic uncertainty dominates.

I previously highlighted the scenario analysis approach in The Bank of England’s Wimbledon Edition, following Governor Bailey’s Jackson Hole speech and ahead of the Bank’s September monetary policy decision. At the recent Bank of England Watchers' Conference, Clare Lombardelli gave her first speech as Deputy Governor for Monetary Policy, where she expanded on this scenario approach in her remarks.

How to Structure Scenario Analysis

Start with the Central Bank's Objective: Identify the primary challenge in achieving the stated objective – for most Central Banks this is in terms of the inflation target (or, for the case of the Federal Reserve, also regarding employment levels).

Develop a Policy Narrative: Create a narrative around the key policy issue. For example, what are the main drivers of inflation?

Build the Scenario Analysis: Map out the qualitative path of the policy rate based on different alternatives tied to the narrative and the transmission mechanism of monetary policy—how changes in the policy rate influence the intended economic outcomes. Typically, three scenarios could offer a comprehensive mapping of alternatives, though two scenarios may be sufficient when uncertainty about the outcome is lower.

To sum up: What is next for Central Banks?

Scenario Analysis as a Focal Point and New Communication Device: it will help coordinate communication among policy committee members.

Pros: Enhances communication, and anchors market expectations with a clear narrative.

Cons: Risks arise if the narrative or the assumed transmission mechanism proves incorrect. This means that it also implicitly requires agreement in terms of monetary policy framework by different committee members. Currently, in major Central Banks, there is little intellectual diversity (the monetary policy reasoning builds on the mainstream New Keynesian model/framework).

Accountability: a byproduct of this approach would be to possibly provide an ex-post framework to evaluate central bank decisions.

In what follows I review the current Bank of England’s scenario analysis and provide a characterization of the Federal Reserve’s one based on Governor Waller’s speech.

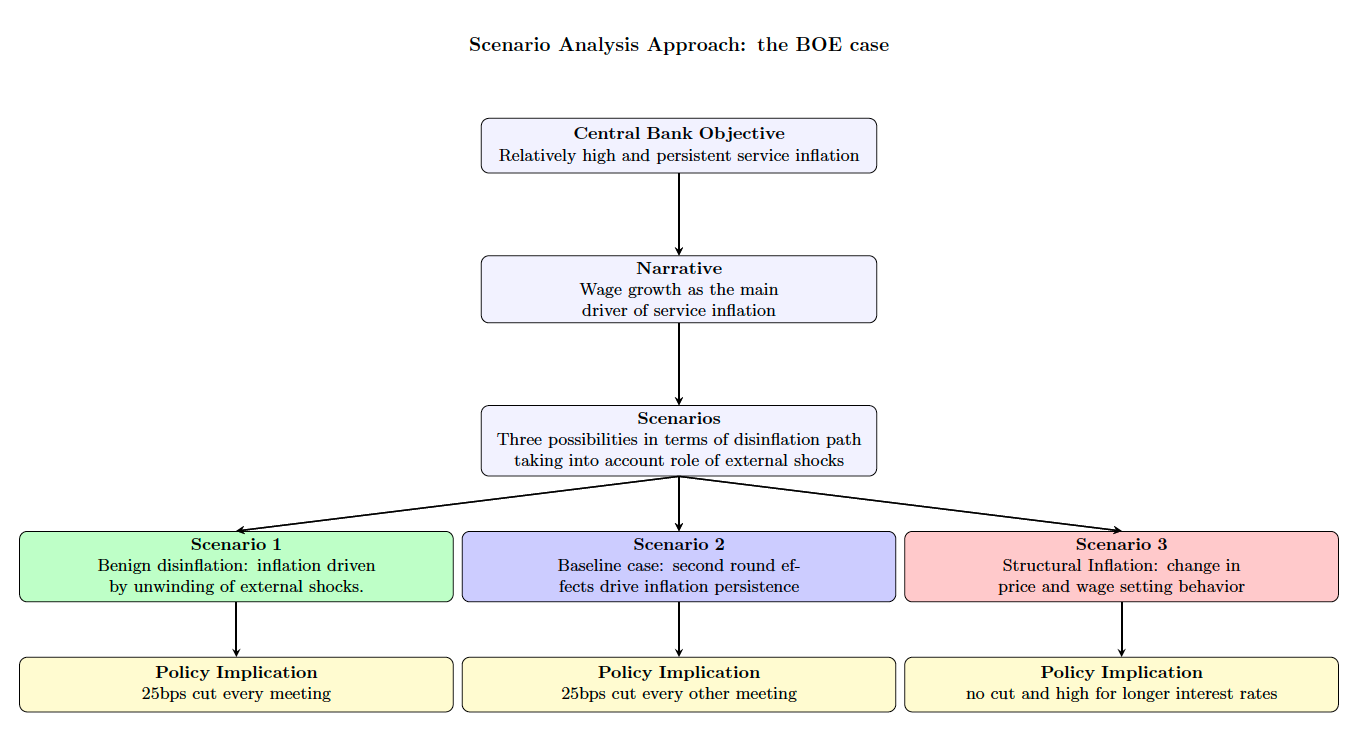

The Bank of England’s Example: The Persistence of Service Inflation

Since August 2024, the Bank of England has taken a clear step in terms of how to design its scenario analysis, partially incorporating Bernanke’s recommendations.

The objective of the Bank of England is to achieve a 2% target in terms of CPI inflation. While headline inflation has been around 2% in the last few months, a key difference from the pre-pandemic period is the persistently high level of services inflation.

Within this context, the Bank's narrative has been focused on the drivers of services inflation. According to its analysis, wages play a significant role in driving services prices up. The relatively slow-moving nature of services inflation is attributed to the "stickiness" of wages, which are less flexible compared to other prices.

Given this background, the Bank of England has set out three scenarios’ outcomes (see Lombardelli’s speech). I will refer to them as benign disinflation, the baseline, and structural inflationary ones.

In the benign disinflation case, “disinflation is driven by the unwind of the external shocks and that will continue to feed through to pay and price setting”.

In the baseline scenario “disinflation is also driven by the unwind of external shocks, but the second-round effects on inflation are more persistent”.

In the structural inflation scenario, “deeper structural changes in the UK economy threaten to impart a more lasting inflationary dynamic”.

The transmission mechanism is based on the premise that restrictive monetary policy1 slows down economic activity, creates output slack, and moderates wage growth. So, the policy path corresponding to the three scenarios could be represented as follows:

Benign Disinflation Scenario: A quicker reduction in monetary policy restrictiveness is needed. I would interpret it as cutting rates by 25 basis points at every meeting.

Baseline Scenario: A gradual removal of restrictive policy is required, which I would interpret as rate cuts of 25 basis points occurring every other meeting to ensure inflation returns to target sustainably.

Structural Inflationary Scenario: Monetary policy must remain restrictively tight for an extended period which I interpret as potentially keeping rates unchanged at their current level.

The Fed’s Initial Attempt to Scenario Analysis: Balancing Risks

In my view, a similar approach to scenario analysis, as seen with the Bank of England, can be found in Waller’s recent speech. I use the October speech as an illustration but in the most recent December speech, he articulates a short-run scenario analysis for the December meeting based on two alternatives and focusing mainly on the behavior of inflation.

The Federal Reserve’s dual mandate focuses on inflation and unemployment, so the narrative would probably balance the risks between these two objectives. In mid-October, following the Fed’s 50-basis-point rate cut in September, the narrative highlighted the tension between two priorities: maintaining a restrictive policy stance to ensure progress toward the 2% inflation target, while avoiding excessive restrictiveness to support full employment and limit rises in unemployment.

Waller outlined a three-scenario approach, which I would classify as the balanced risks scenario (the baseline one), the restrictive policy scenario, and the reacceleration scenario.

In the balanced risks scenario, inflation moves closer to its target while the labor market remains relatively stable. As Waller stated, "The overall strong economic developments that I have described today continue, with inflation nearing the FOMC's target and the unemployment rate moving up only slightly."

In the restrictive policy scenario, a decline in demand results in inflation undershooting its target and weakening labor market conditions. As Waller stated, "Inflation falls materially below 2 percent for some time, and/or the labor market significantly deteriorates."

In the reacceleration scenario, inflation becomes again the concern of the Federal Reserve due to stronger demand that supports employment but may drive additional wage increases: as Waller explained “The third scenario applies if inflation unexpectedly escalates either because of stronger-than-expected consumer demand or wage pressure, or because of some shock to supply that pushes up inflation.”

The transmission mechanism focuses on monetary policy's ability to influence demand, and the underlying FOMC’s consensus is that the current monetary policy stance is restrictive.

Balanced Risks Scenario: Monetary policy would gradually reduce its restrictiveness at a steady pace, likely interpreted as 25-basis-point cuts at each meeting. As Waller stated, "This scenario implies to me that we can proceed with moving policy toward a neutral stance at a deliberate pace." He added, "In this circumstance, our job is to keep inflation near 2 percent and not slow the economy unnecessarily."

Restrictive Policy Scenario: The Federal Reserve would need to cut rates more aggressively to reach the neutral rate quickly. Waller noted, "The message here is that demand is falling, the FOMC may suddenly be behind the curve, and that message would argue for moving to neutral more quickly by front-loading cuts to the policy rate."

Reacceleration Scenario: The Federal Reserve would pause the rate-cutting cycle, maintaining the policy rate at its current level. According to Waller, "In this circumstance, as long as the labor market isn't deteriorating, we can pause rate cuts until progress resumes and uncertainty diminishes."

Conclusions

Scenario analysis could offer a valuable tool for central banks to enhance transparency and clarify how they interpret and address policy challenges. By presenting a structured narrative, it can help anchor market expectations and guide public understanding of monetary policy decisions.

However, the effectiveness of this approach relies on two key factors:

Choosing the right narrative;

Accurately assessing the transmission mechanism.

One important aspect of the scenario analysis is that it might require flexibility in terms of adapting the narrative to new developments. Especially, the current economic landscape is characterized by geopolitical and structural shifts (e.g. related to immigration, trade, productivity developments) that would demand macro adaptability.

The monetary policy stance is restrictive when the real interest rate exceeds the neutral real interest rate (i.e., when R-R*>0). See blog post Has the Fed Monetary Policy been Restrictive? for further details.

In principle, providing scenarios would be a step forward, but...

A) a CB should have a policy to have a narrative. For over a year both the Fed and the ECB have been repeating ad nauseam they are data driven. Let me translate: clueless.

From the transitory mantra on, the show has been despicable

B) It is a complex world. Having lawyers manage monetary policy is nothing less than masochistic. Did you hear any Powell'd press conference? The sense of void is overbearing. The guy has one of the most important jobs in the world and is unfit. Just in case the detail was overlooked, the temporary thing was buying time while he was being confirmed by Biden

He did not want to do anything that could have threatened his confirmation. Good luck explaining that in a scenario

C) is there any agreement on the neutral rate? Nope, sorry.

D) inflation itself should be redefined. If profits drive the stock price increases, it is fine. When multiples explode and get to the same outcome, it is inflationary

If real estate prices grow 30 to 40% in two years, it is inflationary.

We should stop claiming the increasing asset prices are good and the increasing labor costs bad. It is just people trying to buy a home.

It is discriminatory and leads to all the turmoil we are witnessing in the Western world