Japan February-25 CPI Inflation Report

Inflation just above market expectations supports gradual normalization cycle by the Bank of Japan.

Key takeaways:

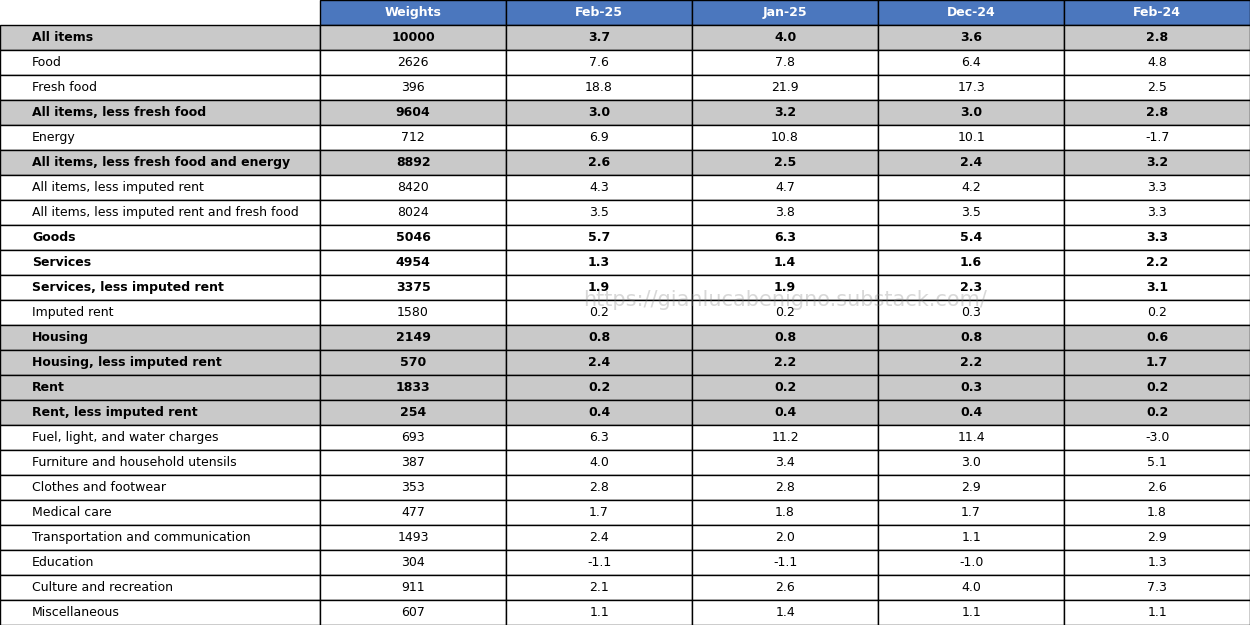

Japan's Consumer Price Index (CPI) increased by 3.7% year-on-year (YoY) in February, lower than the 4.0% rise observed in January but higher than market expectations of a 3.5% increase.

CPI excluding fresh food, the Bank of Japan's preferred measure, rose by 3.0% YoY in February, above market expectations of a 2.9% YoY increase, and below January’s 3.2% increase.

Similarly, CPI excluding fresh food and energy rose by 2.6% YoY in February, compared to January’s figure of 2.5% YoY.

Fresh food inflation has been a prominent issue in Japan for several months. In February, fresh food prices surged by 18.8% year-over-year, with rice inflation reaching 80.9% YoY—marking the fifth consecutive month above 50% YoY. Meanwhile, fresh vegetable prices rose by 28.0% YoY, and fresh fruit prices increased by 20.0% YoY.

Japan's inflation diverges from patterns seen in other advanced economies. It is primarily driven by the goods sector, which rose by 5.7% YoY in February (versus 6.3% YoY in January), rather than by the services sector, which saw a minor 1.3% YoY rise in February, following January’s 1.4% YoY increase. The Yen’s depreciation over the last quarter (and in 2024 as a whole) has been a key driver of goods inflation in the country given the pass-through effect on imported costs.

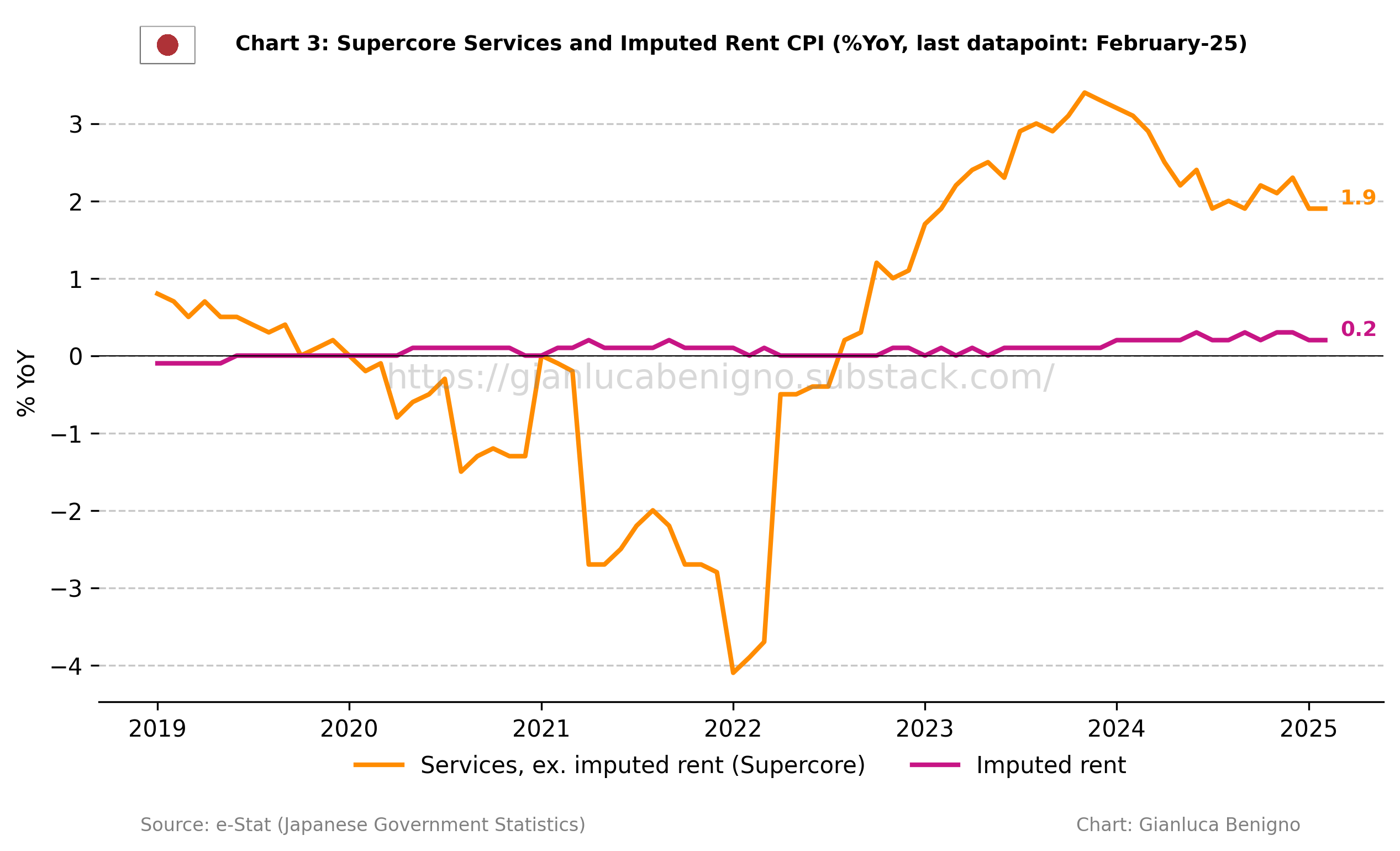

Inflationary pressures at the level of service inflation seem to be consolidating around 2% for service inflation less imputed rent (increasing by 1.9% YoY in February, the same increase as in January 2025 but lower than December’s increase of 2.3% YoY).

The BOJ decision, announced on March 18-19, was no surprise, holding its policy rate at 0.5%, with markets pricing in the next rate hike later in the year. However, the persistence of core inflation (excluding food and energy) above 2%, along with its reacceleration since mid-2024 and positive nominal wage negotiations could increase pressure on the Bank of Japan to adjust the pace of its interest rate hikes.

Related Posts

Japan January 25 Inflation Report (previous release)

Japan December 24 Inflation Report (previous release)

Japan November 24 Inflation Report (previous release)

Japan October 24 Inflation Report (previous release);

Japan September-24 Inflation Report (previous release);

Japan August-24 Inflation Report (previous release);

A Quasi-Global Inflation Overview (related post);

The Bank of Japan's Put (related post);

Post-FOMC Update: The Fed and the Market Shifts (related post).

Review of the Inflation Release

In February 2025, consumer prices increased by 3.7% year-on-year (YoY), above the consensus expectation of a 3.5% increase, but lower than the 4.0% YoY reported in January. On a month-on-month basis (MoM), prices decreased by 0.4% in February, compared to January’s 0.5% MoM increase.

Regarding core measures, the Bank of Japan tracks two main core inflation metrics (Chart 1): The Consumer Price Index (CPI) excluding fresh food, and the CPI excluding fresh food and energy.

The first measure, which excludes fresh food, increased by 3.0% YoY in February, above market expectations of a 2.9% YoY rise, and below the 3.2% YoY increase recorded in January. On a month-to-month (MoM) basis, February’s figure decreased by 0.1% MoM, compared to January’s 0.2% MoM increase.

The second core measure, excluding fresh food and energy, rose by 2.6% YoY, slightly higher than the 2.5% YoY increase in January. On a month-to-month basis, core prices rose by 0.2% MoM, compared to the 0.1% MoM increase recorded in January. Energy prices, a more volatile component by nature, are still consistently driving up inflation in the country: energy prices increased by 6.9% YoY in February, down from January’s increase of 10.8% YoY.

In contrast to many advanced economies, where the services sector is still the main driver of inflation, Japan’s inflation is predominantly fueled by goods inflation (Chart 2). In February, the Goods CPI increased by 5.7% YoY, compared to the 6.3% YoY increase recorded in January. In contrast, the Services CPI rose by 1.3% YoY, slightly below the 1.4% YoY increase in January.

On a month-on-month basis (MoM), goods inflation decreased by 0.8% in February, a reversal of the 1.0% MoM January’s increase. Conversely, service inflation increased by 0.1% MoM, compared to January’s 0.1% MoM decrease.

Further emphasizing Japan's unique position, the shelter component (“imputed rents”) of the CPI increased by 0.2% YoY in February, the same increase as in January 2025. The “imputed rents" measure represents “the rent a person would have to pay to own and occupy a property”, which constitutes the largest part of the CPI's housing component and weighs about 16% of the overall CPI. For a detailed breakdown of Japan's housing and rent components, refer to Tables 1 and 2.

In Tables 1 and 2, we provide a more detailed breakdown of the components of CPI, including CPI inflation excluding imputed rents (Chart 4), which we consider the HICP-equivalent CPI. This measure facilitates international comparisons across countries and blocs, a methodology developed by the European Union Statistical Office. In February, HICP inflation rose by 4.3% YoY versus January’s 4.7% increase. As Chart 4 shows, HICP inflation peaked at the beginning of 2023, reaching just above 5%. In contrast, before the pandemic, HICP inflation fluctuated between 0% and 1% year-over-year.

Policy Implications

Inflation trends continue to support the normalization cycle initiated by the Bank of Japan last year. Headline inflation, core CPI (excluding fresh food), and CPI excluding fresh food and energy have all comfortably exceeded the 2% target. Notably, from the BOJ’s perspective, a key positive development has been the stabilization of service inflation above 1% since Q4 2024—a significant and welcome shift from pre-pandemic levels. Combined with wage negotiations that have shown an average wage increase above 5% for both large and small and medium-sized corporations, the current release supports further increases in interest rates by the Bank of Japan. As in other jurisdictions, risks to the monetary policy outlook are also related to trade policy developments.

Table 1: CPI by components (% YoY)

Source: e-Stat (Japanese Government Statistics)

Table 2: CPI by components (% MoM)

Source: e-Stat (Japanese Government Statistics)