Switzerland February-25 CPI Inflation Report

Disinflation persists and validates expectations of 25bps cut by the SNB

Key takeaways:

In February 2025, the Swiss Consumer Price Index (CPI) rose by 0.3% year-on-year (YoY), slightly lower than January’s 0.4% YoY increase and in line with the consensus forecast of 0.3% YoY. On a month-on-month (MoM) basis, the CPI rose by 0.6% in February – slightly up from consensus forecasts of 0.5% MoM –and significantly higher than January’s 0.1% decline.

Core CPI increased by 0.9% YoY in February, the same as in January. On a month-on-month basis (MoM), core CPI increased by 0.7% MoM in February, a significant increase from January’s 0.1% MoM decline.

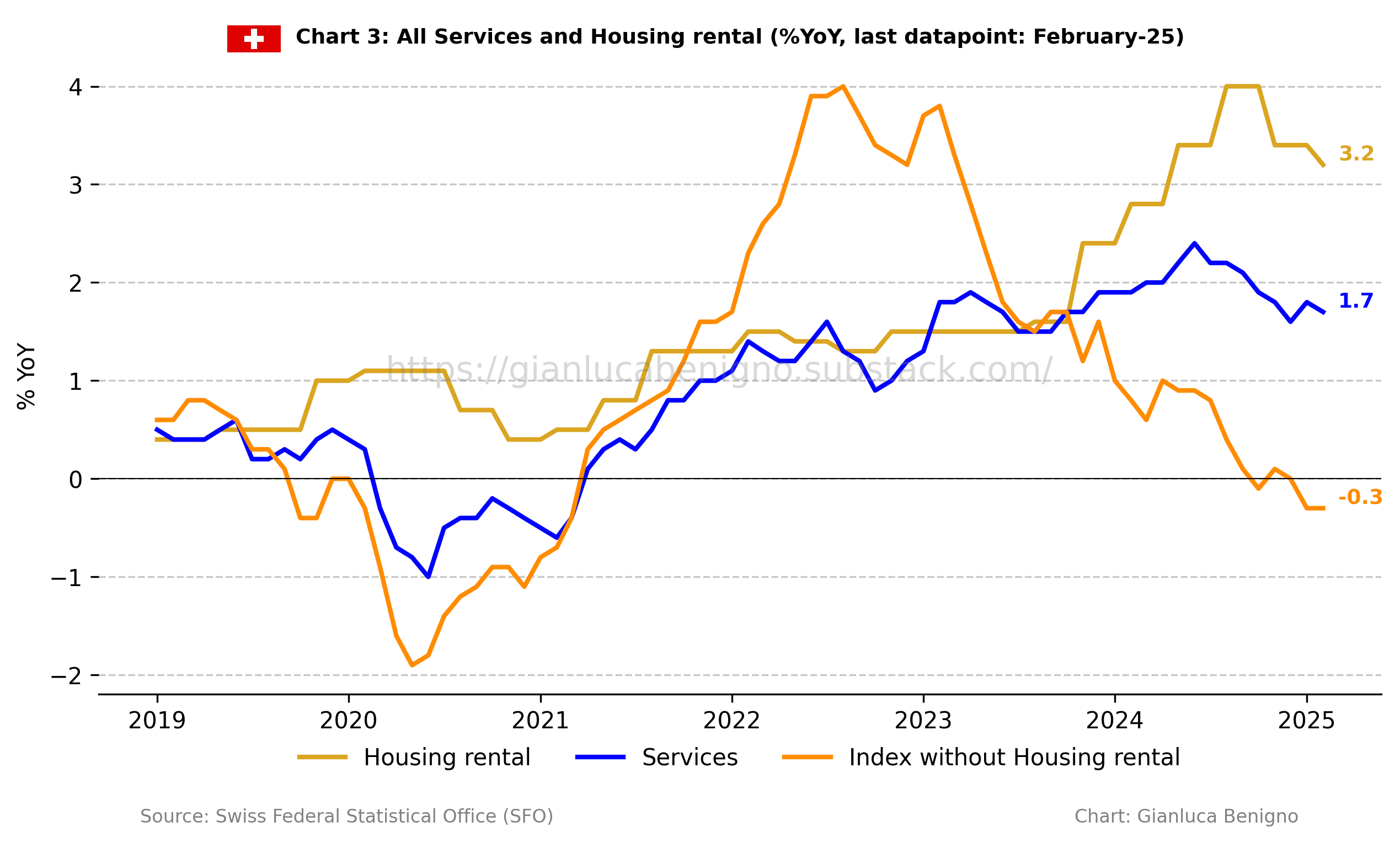

The services sector was the primary driver of rising prices, experiencing a 1.7% YoY increase in February, slightly lower than January’s 1.8% YoY figure. In contrast, the goods sector declined by 1.8% YoY in February, in line with the 1.8% YoY decrease in January.

As noted in past reports, the February CPI update includes new data on housing rentals, which is adjusted every three months. Compared to the previous 3.4% YoY increase recorded in November, December, and January, the housing rental component rose by 3.2% YoY in February.

These results are consistent with a common dichotomy faced by Central Banks in (major) advanced economies: goods prices are in a deflationary territory while service price inflation is slowly adjusting.

A parallel dichotomy arises in Switzerland by examining import and domestic prices, with import prices declining by 1.5% YoY in February (same as in January) and domestic prices rising at 0.9% YoY (versus 1.0% YoY in January and 1.5% in December).

From the SNB's perspective, the current release and the January release confirm the disinflationary outlook that has led to the further downward revision of the conditional inflation path outlined in its latest monetary policy assessment.

Excluding housing rentals, the CPI inflation declined by 0.3% YoY in February, once again, in line with the January reading (-0.3% YoY) and the no change (0% YoY) from December.

Related Posts

Switzerland January 25-CPI Inflation Report (previous release)

Switzerland December 24 -CPI Inflation Report (previous release)

Switzerland November 24-CPI Inflation Report (previous release)

The SNB’s Forward-Looking Compromise (analysis of SNB’s September policy decision)

The SNB’s Challenging Rebalancing Act (analysis of SNB policy and Catch-22 effect for the SNB)

The SNB sets the time (analysis of SNB policy and Catch-22 effect for the SNB)

Review of the Inflation Release

Consumer prices rose by 0.3% year-on-year (YoY) in February 2025, versus January’s increase of 0.4% YoY, and in line with the consensus forecast of 0.3% YoY. On a month-on-month (MoM) basis, consumer prices increased by 0.6%, following a 0.1% MoM decline in January.

Core CPI, which excludes fresh and seasonal products as well as energy and fuels, increased by 0.9% year-on-year (YoY) in February (Chart 1), which was the same as the 0.9% YoY increase in January. On a month-on-month basis, Core CPI increased by 0.7% MoM in February, a significant change from the 0.1% MoM decline from January.

Similarly to trends seen in other advanced countries, the services sector, rather than the goods sector, is the main driver of rising prices (Chart 2). In February, services saw a 1.7% YoY increase, modestly down from the 1.8% recorded in January. Meanwhile, the goods sector experienced a decline of 1.8% YoY, in line with the 1.8% YoY decrease recorded in January.

Upon examining the more disaggregated data (refer to Tables 1 and 2), it is evident that, like other advanced economies, housing rentals are the primary driver of inflation (as shown in Chart 3). In Switzerland, this component of the Consumer Price Index (CPI) is adjusted every three months, and in February, housing rentals experienced an increase of 3.2% YoY, down from the previous quarter’s (November- December- January) 3.4% YoY increase. As noted previously, the dynamic of the housing rental component is strictly connected with the policy rate. As the policy rate has been lowered in the past year, it is not too surprising to observe a decline in this component since its peak of August-September and October’s reading. Nonetheless, this component remains an important driver of inflation at the CPI level. Thus, excluding housing rentals, the CPI index decreased by 0.3% YoY in February, in line with the 0.3% YoY decline in January and the no change (0%) reported in December.

Another important classification from Switzerland's perspective is the distinction between domestic and imported inflation (see Chart 4). In February, domestic inflation rose by 0.9% year-on-year, slightly lower than the 1.0% YoY recorded in January. On a monthly basis, domestic inflation increased by 0.5% MoM versus the 0.1% increase in January. In contrast, imported inflation decreased by 1.5% YoY in February, mirroring the 1.5% decline recorded in January. On a monthly basis, imported inflation increased by 0.9% in February – a significant change from the -0.7% observed in January.

The Swiss Federal Statistical Office also makes available a measure of the Harmonized Price Index of Consumer Prices (The Harmonized Index of Consumer Prices (HICP) is an indicator that the member states of EU and EFTA calculate based on a harmonized method and allows for international inflation comparisons). In February, the HICP increased by 0.1% on a year-on-year basis, slightly lower than January’s 0.2% YoY reading.

Summary

The report presents a similar disinflationary outlook as the previous releases. In addition to the ongoing deflationary trend in goods and the effects of imported inflation, it's important to highlight the decline in domestic inflation, down from 1.0% YoY in January to 0.9% YoY in February. The higher monthly reading at the core and domestic inflation levels are mainly driven by the increase of the housing rental component on a monthly basis (0.7% MoM).

An additional indicator of the almost deflationary context is the behavior of CPI inflation, excluding housing rentals. In February, this measure decreased by 0.3% YoY, as it did in January (-0.3% YoY), and was lower than December’s no-change (0%).

The next monetary policy decision by the Swiss National Bank is in March. It is widely expected that the SNB will cut the policy rate by 25bps. The current release supports this expectation.

Table 1: CPI by components (% YoY)

Source: Swiss Federal Statistical Office (FSO).

Table 2: CPI by components (% MoM)

Source: Swiss Federal Statistical Office (FSO).