UK June-25 CPI Inflation Report

Inflation came in above expectations at both the headline and core levels, with no improvement in service inflation compared to last month.

Key takeaways:

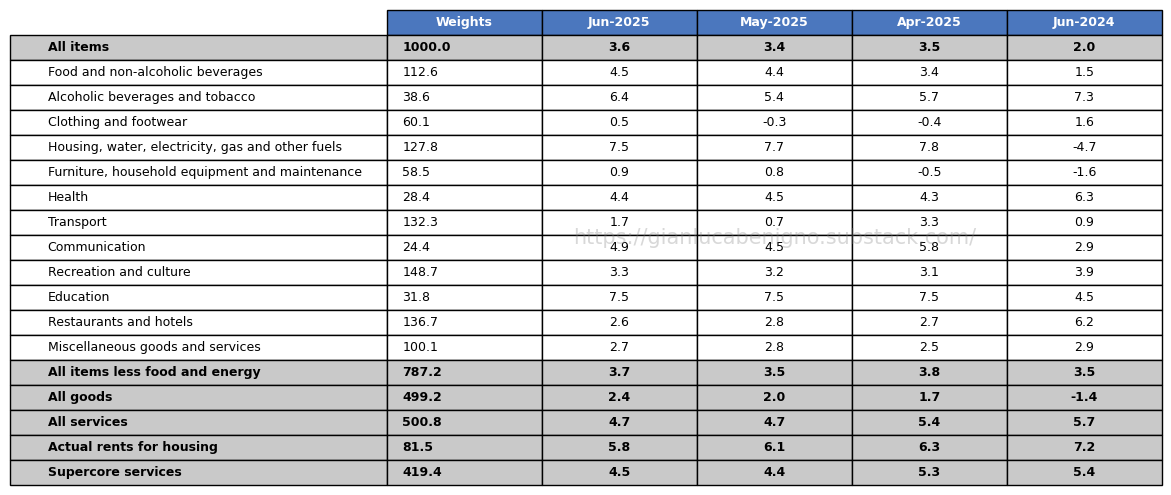

UK Consumer Price Index (CPI) increased by 3.6% year-on-year (YoY) in June, above May’s figure at 3.4% YoY, and the market consensus of 3.4% YoY.

Core CPI in June increased by 3.7% YoY, above the consensus forecast of 3.5% YoY, and above May’s 3.5% YoY increase.

Consistent with the trend in other advanced economies, inflationary pressures remain primarily concentrated in the services sector, which saw an increase of 4.7% YoY in June, the same reading as in May. Meanwhile, inflation in the goods sector is now rising at 2.4% YoY, higher than May’s increase of 2.0% YoY.

Elevated housing costs remain the primary driver of inflation within the services sector. In June, actual rents rose by 5.8% year-on-year, down from 6.1% in May. As noted in the previous report, the ongoing moderation in this component is to be expected, given earlier price increases and the decline in interest rates since August 2024.

Our supercore service inflation (which removes actual rents for housing from services CPI) increased by 4.5% YoY in June, higher than May’s 4.4% YoY increase.

Overall, the inflation outlook is above the Bank of England’s latest forecast of 3.3% year-on-year for Q2, based on current interest rates (as outlined in the May Monetary Policy Report). The current elevated reading reflects a combination of persistently slow adjustment in service inflation and rising goods inflation now well above 2% YoY.

The next MPC meeting is scheduled for early August, with money markets having priced in a high probability of a 25 basis point cut, before the latest inflation data, as key officials had highlighted the risk of emerging economic slack. However, the current inflation release may lead to a split vote within the Committee, with some members potentially preferring to keep the Bank Rate unchanged.

Related Posts

UK May-25 CPI Inflation Report (previous release)

UK April-25 CPI Inflation Report (previous release)

UK March-25 CPI Inflation Report (previous release)

UK February-25 CPI Inflation Report (previous release)

UK January-25 CPI Inflation Report (previous release)

UK December-24 CPI Inflation Report (previous release)

The Flip Side of Monetary Policy (related post)

The Bank of England at a Crossroads: Rethinking the Narrative Before It’s Too Late? (related post)

Scenario Analysis as a Communication Device for Central Banking (related post)

A Quasi-Global Inflation Overview (related post)

Has Wage Growth Fueled Inflation in the UK? (related post)

At the Core of UK Inflation (construction of supercore inflation and supercore wage index)

FT Alphaville on Catch-22 (short version of the Catch-22 effect)

Is the Bank of England in a Catch-22 Situation (long version of the Catch-22 effect)

Review of the Inflation Release

In June 2025, consumer prices increased by 3.6% year-on-year (YoY), above the market consensus of 3.4% and higher than May’s figure of 3.4% YoY. On a month-on-month (MoM) basis, consumer prices increased by 0.3%, higher than the 0.2% MoM increase recorded in May.

Core CPI, which excludes food and energy, rose by 3.7% YoY, above the consensus forecast of 3.5% YoY, and May’s 3.5% YoY increase (see Charts 1 and 2). On a month-on-month basis, core CPI increased by 0.4%, higher than the 0.2% MoM increase recorded in May.

The services sector remains the primary driver of inflation, with an increase of 4.7% YoY in June, the same reading as in May. On a monthly basis, service inflation rose by 0.6% MoM, higher than the 0.1% MoM decline observed in May. The goods sector inflation showed a 2.4% YoY increase in June, higher than the 2.0% increase observed in May. On a month-on-month basis, goods inflation was unchanged at 0.0% MoM, compared to the 0.4% MoM increase recorded in May. Chart 3 highlights the persistence of service inflation and the upward trend in goods price inflation, which is now adding to overall inflation rather than offsetting it, as it did for most of 2024.

A distinctive feature of inflation developments in the UK has been the ongoing rise in housing inflation (what we refer to as the “Catch-22” effect, see also “The Flip Side of UK Monetary Policy”), which has been the primary driver of inflationary pressures (Table 1). Actual rents for housing rose by 5.8% YoY in June, lower than May’s 6.1% YoY increase, April’s 6.3% YoY increase, and March’s 7.2% YoY increase, indicating a clear declining path following the upward trend of actual rents for housing seen since September 2021. Given that interest rates peaked between August 2023 and August 2024, and following the logic of the Catch-22 effect, where higher rates initially fuel rent increases, it is reasonable to expect a continued decline in actual rent inflation through 2025. On a month-to-month basis, actual rents rose by 0.2% MoM in June, compared to 0.2% MoM in May and 0.3% MoM in April.

Our measure of supercore services inflation rose by 4.5% year-on-year in June, up from 4.4% in May. On a monthly basis, it increased by 0.7%, reversing the 0.1% decline recorded in May.

Summary and Policy Implications

At its meeting ending on 18 June 2025, the Bank of England left the Bank Rate unchanged at 4.25%. The next MPC meeting is scheduled for early August, and money markets are currently pricing in a high probability of a 25 basis point cut.

One key concern raised by Bank of England officials is the possibility that further slack may be emerging in the economy. Recent economic activity data have been discouraging, with GDP unexpectedly contracting by 0.1% in May, driven by sharp declines in manufacturing and construction. This followed a 0.3% drop in April, marking the second consecutive month of economic contraction.

On the inflation front, the Bank of England has highlighted the path of service inflation and nominal wage growth as key risks. After the anticipated April increase—driven by indexed and regulated prices—service inflation showed no further improvement in June relative to May, despite continued moderation in housing rental inflation. Our supercore services index also edged slightly higher, consistent with the overall slow adjustment in the broader services category.

The overall inflation outlook appears less favorable than the trajectory projected in the May Monetary Policy Report. Given the potential increase in downside risks to the economy, the likelihood of a 25 basis point cut will depend on how the MPC balances inflation concerns against the weakening economic outlook, raising the possibility of a split vote at the upcoming meeting.

Table 1: CPI by components (% YoY)

Source: UK Office of National Statistics (ONS).

Table 2: CPI by components (% MoM)

Source: UK Office of National Statistics (ONS).